Accurate inventory records can help businesses to make informed decisions, improve financial performance, and comply with tax reporting requirements. Compare the physical inventory counts with the recorded inventory levels in the accounting system. Calculate the total value of the discrepancies to determine the necessary adjustments. These records include invoices, receipts, and any other documentation related to inventory purchases. Purchase records help verify the inventory acquired during the period and ensure that all purchases are accurately recorded in the accounting system. Inventory is a key component of a company’s current assets on the balance sheet.

- Inventory management is one of the essential aspects of business management.

- When an item is ready to be sold, transfer it from Finished Goods Inventory to Cost of Goods Sold to shift it from inventory to expenses.

- This method smooths out price fluctuations over the accounting period by averaging the cost of beginning inventory and purchases.

- By following these best practices and tips, businesses can maintain accurate inventory records, improve operational efficiency, and enhance financial performance.

Accounting for Inventory (Purchase, Journal Entries, Example, and More)

These adjustments help in presenting a true picture of the company’s financial health and operational efficiency. This article has outlined the essential steps for making adjusting journal entries for inventory accounts. These steps include gathering necessary information, calculating adjustments, preparing the journal entry, and reviewing and approving adjustments. Detailed examples have been provided for common scenarios such as adjusting for physical inventory counts, inventory shrinkage, obsolete inventory, and consignment inventory.

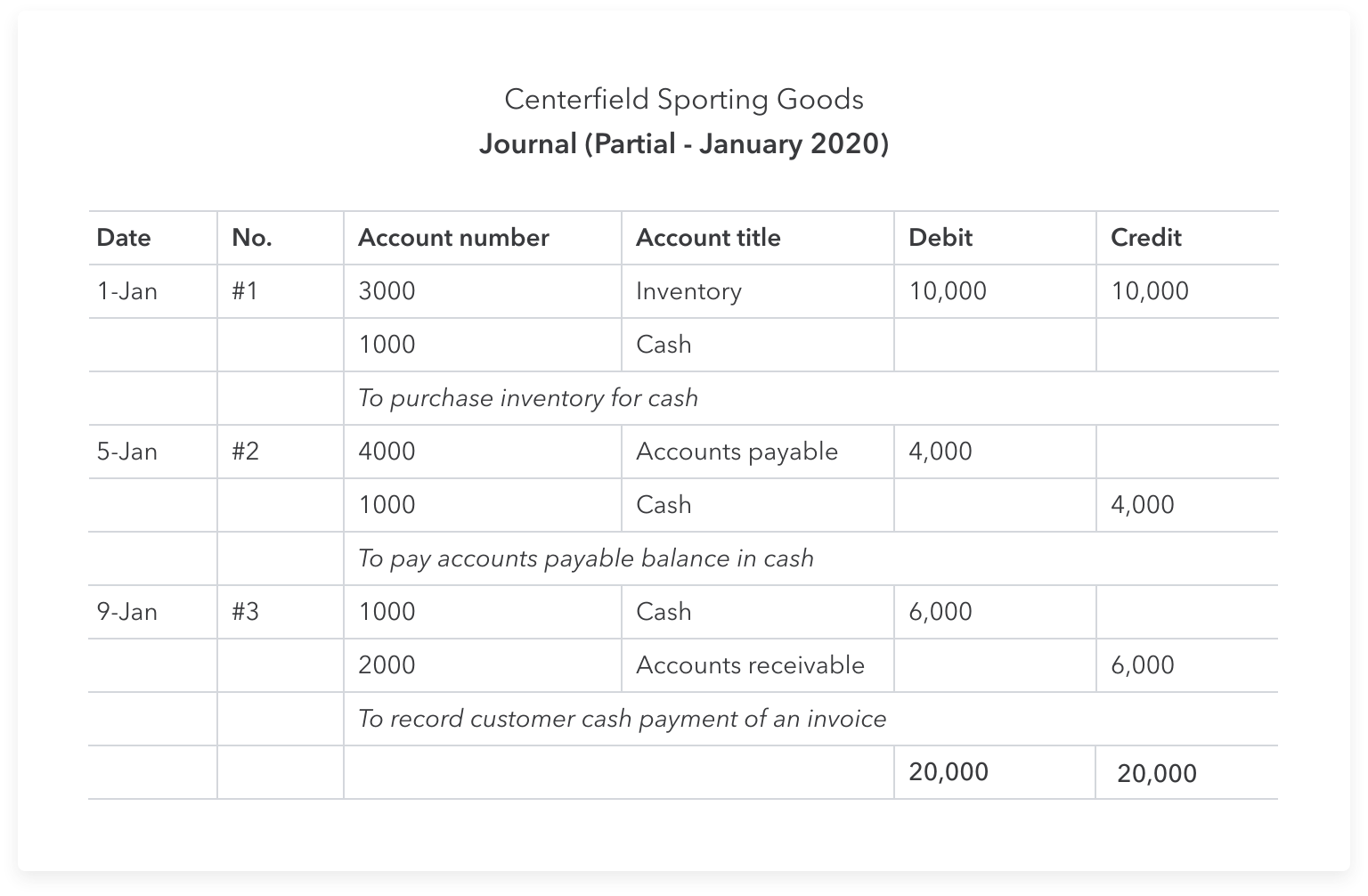

Best Practices for Recording Journal Entries

Debiting the Inventory account increases Garden Supplies Co.’s assets, as it adds value to the company’s stock. Crediting the Accounts Payable account increases the company’s liabilities, showing that the purchase will be paid for at a later date, not immediately impacting the company’s cash flow. An inventory write-down and write-off are two common accounting adjustments to inventory that reduce the carrying value of inventory on the balance sheet. But while the circumstances for both share commonalities, one particular distinction must be understood. Under U.S. GAAP accounting standards (FASB), the lower of cost or market (LCM) rule is used to value inventories. The LCM rule states that the inventory carrying balance recorded must reflect the lesser value of the original cost or current market value.

Is the purchase of inventory always recorded as an increase in assets?

By relying on digital technologies, perpetual inventory systems reduce the need to physically count a company’s inventory. Both merchandising and manufacturing companies can benefit from perpetual inventory system. When inventory is purchased on credit, the Inventory account on the balance sheet increases, reflecting more assets, and the Accounts Payable account also increases, indicating a rise in liabilities.

The raw materials entry also accounts for the movement of raw materials within your warehouse, allowing you to track when your production materials are moved from storage into production. The lower-of-cost rule states that a business inventory accounting journal entry must record inventory at the lower of cost. Undertake a physical inventory count at the end of the accounting period to determine the exact quantities of inventory on hand.

Debit your Raw Materials Inventory account to show an increase in inventory. Your business’s inventory includes raw materials used to create finished products, items in the production process, and finished goods. There are key differences between perpetual inventory systems and periodic inventory systems. The journal entries used when bookkeeping in the perpetual inventory system are different compared to the ones used in a periodic system. Accountants don’t have to constantly adjust the changes in inventory levels since everything is done by the computing system (for the most part). For example, optical scanners are used in markets to keep track of inventory quantities, but at the end of the accounting period, a physical inventory is performed.

However, the company already record inventory write down $ 5,000 for the whole inventory, which already impacts income statement. So this actual damage will not impact income statement but the inventory reserve. Although there is an increase in accounts payable or cash out here, the cost has not occurred yet. By following these steps, you can create an accurate inventory journal entry to reflect the transaction and maintain accurate accounting records. The Weighted Average Cost method calculates an average cost for all inventory items available during the period.

With periodic inventory, you update your accounts at the end of your accounting period (e.g., monthly, quarterly, etc.). A perpetual inventory system keeps continual track of your inventory balances. Not to mention, purchases and returns are immediately recorded in your inventory accounts. tax returns By meticulously recording inventory purchases, a business can maintain accurate financial records, essential for analyzing its financial health, making informed decisions, and reporting to stakeholders. Inventory purchases represent the acquisition of goods that a business intends to sell.