If DenimWorks pays more than $8,400 for the year, there is an unfavorable budget variance; if the company pays less than $8,400 for the year, there is a favorable budget variance. This could be for many reasons, and the production supervisor would need to determine where the variable cost difference is occurring the fixed overhead spending variance is calculated as: to better understand the variable overhead efficiency reduction. Sometimes these flexible budget figures and overhead rates differ from the actual results, which produces a variance. Similarly, an adverse or unfavorable variance arises when the actual costs incurred are higher than the budgeted costs.

Fixed Overhead Spending Variance Formula

This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Finance Strategists has an advertising relationship with some of the companies included on this website.

Fixed Overhead Volume Variance

We will discuss how to report the balances in the variance accounts under the heading What To Do With Variance Amounts. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. As shown in the example above, Tahkila Industrial had a favorable variance for the year ended 2019 since they had to pay $80,000 less than expected. Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping.

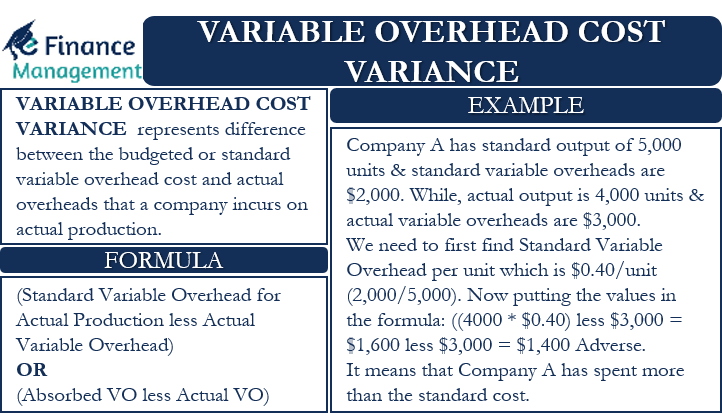

Determination of Variable Overhead Efficiency Variance

In a standard cost system, overhead is applied to the goods based on a standard overhead rate. The standard overhead rate is calculated by dividing budgeted overhead at a given level of production (known as normal capacity) by the level of activity required for that particular level of production. Therefore, these variances reflect the difference between the Standard Cost of overheads allowed for the actual output achieved and the actual overhead cost incurred. However, during the period cost rationalization measures were carried out and fixed overheads were reduced by minimizing inefficiencies resulting in an annual fixed overhead expense of $420,000. In this article, we will cover in detail about the fixed overhead spending variance.

Fixed Overhead Expenditure Variance, also known as fixed overhead spending variance, is the difference between budgeted and actual fixed production overheads during a period. The credit balance on the fixed overhead budget variance account (2,000), has now been split between the work in process inventory account (600) and the cost of goods sold account (1,400) decreasing both accounts by the appropriate amount. The debit balance on the fixed overhead volume variance account (1,040) has been charged to the cost of goods sold account, and both variance account balances have been cleared. (c) In addition, prepare a reconciliation statement for the standard fixed expenses worked out at a standard fixed overhead rate and actual fixed overhead.

Determination of Variable Overhead Rate Variance

- Fixed Overhead Spending Variance is calculated to illustrate the deviation in fixed production costs during a period from the budget.

- As an example of an unfavorable fixed overhead spending variance, a passing tornado delivers a glancing blow to the production facility of Hodgson Industrial Design, resulting in several hundred roofing tiles being blown off.

- The fixed manufacturing overhead volume variance is the difference between the amount of fixed manufacturing overhead budgeted to the amount that was applied to (or absorbed by) the good output.

- Motors PLC is a manufacturing company specializing in the production of automobiles.

Standard fixed overhead costs are allocated to production based on the standard rate which is calculated using the budgeted production volume. If the actual production volume is not the same as the budgeted production volume then there will be a variance between the budgeted fixed overhead and the standard fixed overhead. Two variances are calculated and analyzedwhen evaluating fixed manufacturing overhead. The fixedoverhead spending variance is the difference between actualand budgeted fixed overhead costs. The fixed overheadproduction volume variance is the difference between budgetedand applied fixed overhead costs. The standard overhead rate is the total budgeted overhead of \(\$10,000\) divided by the level of activity (direct labor hours) of \(2,000\) hours.

Using the information given below, compute the fixed overhead cost, expenditure, and volume variances. A portion of these fixed manufacturing overhead costs must be allocated to each apron produced. This is known as absorption costing and it explains why some accountants say that each product must “absorb” a portion of the fixed manufacturing overhead costs. Usually, the level of activity is either direct labor hours or direct labor cost, but it could be machine hours or units of production. Actual production volume is the production that the company actually achieves (in hours) or produces (in units) during the period.

We commonly call The fixed overhead spending variance as fixed overhead expenditure variance or fixed production overhead expenditure variance. Before going further detail, let’s have a look at overview and the basic definition. The fixed overhead production volume variance is favorablebecause the company produced and sold more units thananticipated. Adverse fixed overhead expenditure variance indicates that higher fixed costs were incurred during the period than planned in the budget.

If the actual production volume is higher than the budgeted production, the fixed overhead volume variance is favorable. On the other hand, if the actual production volume is lower than the budgeted one, the variance is unfavorable. This is a cost that is not directly related to output; it is a general time-related cost.

This could be for many reasons, and the production supervisor would need to determine where the variable cost difference is occurring to better understand the variable overhead reduction. This example provides an opportunity to practice calculating the overhead variances that have been analyzed up to this point. Variance analysis is the process of identifying and quantifying the differences between actual and budgeted or standard performance measures, such as costs, revenues, or quantities. This could be for many reasons, and the production supervisor would need to determine where the variable cost difference is occurring to make production changes. In August, the company ABC which is a manufacturing company has produced 950 units of goods in the production.

Businesses often give more importance to ADVERSE variances than FAVORABLE variances. Initially the actual fixed overhead expense (rent etc) would have been posted to the expense account with the usual entry of debit expense, credit accounts payable (not shown). The journal above now allocates some of this expense (11,000) to production, this is represented by the credit entry to the expense account.